Official reserve shifts and ETF inflows lift demand for gold vs dollar. Watch central bank flows, ETF volumes, the dollar and US real yields.

Gold rose 37% YTD in 2025 as central banks and investors stepped in.

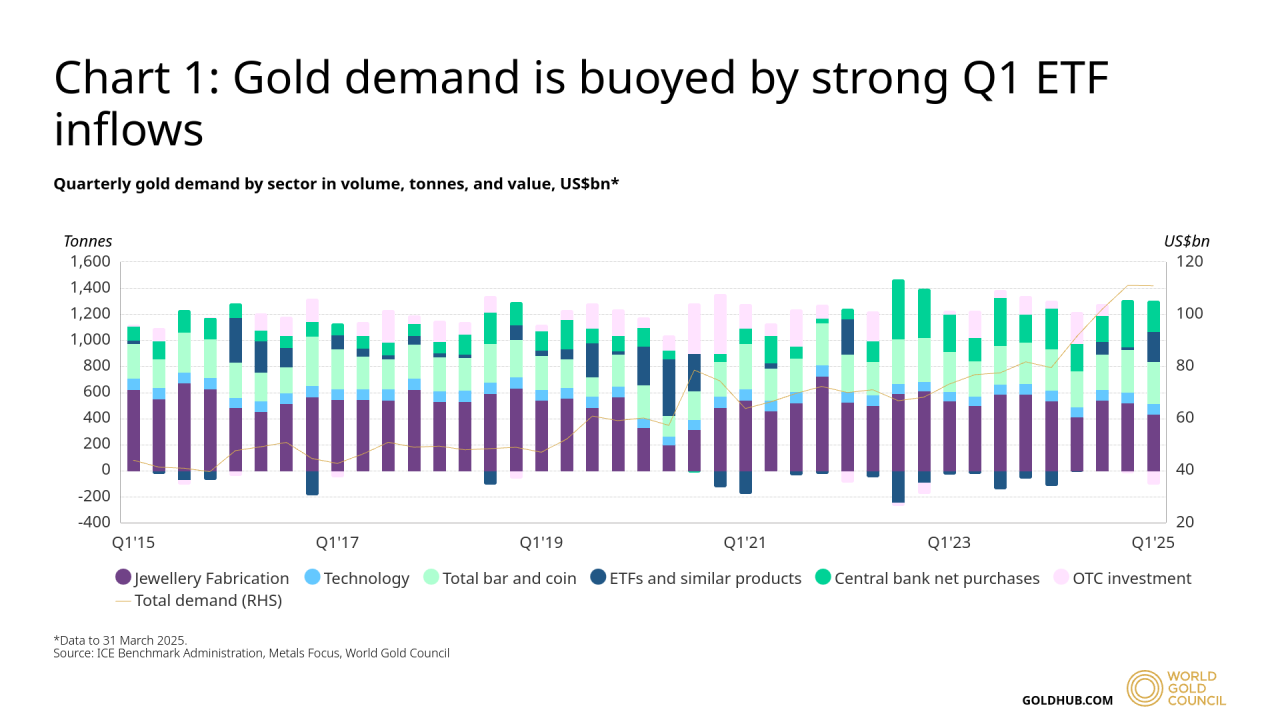

Official buyers purchased 244 tonnes in Q1, while physically backed ETFs took in US$5.5bn in August. A weaker dollar and falling US real yields make gold more attractive to reserve managers and private investors around the world, fueling its current growth.

RELATED: Trump’s Fed Threat Could Spark Gold Rally, Says BofA

Institutional Demand: Central Banks & ETFs

Official demand for gold looks structural. Central banks bought 244 tonnes in Q1 2025, about 25% above the five-year quarterly average, with notable purchases from China and the National Bank of Poland.

Physically backed ETFs also moved materially; global gold ETFs attracted US$5.5bn in August, roughly 53 tonnes equivalent, with North America supplying most flows.

Those combined official and investor purchases have persisted over several months, tightening available above-ground supply significantly.

ALSO READ: UBS Sees Macro Forces Driving Gold Prices To $3,700 By Mid 2026

De-Dollarization Mechanics: China, Russia, BRICS And Reserve Strategy

Reserve diversification is active. The People’s Bank of China added gold for its ninth straight month in July and for a tenth month in August, signaling steady accumulation.

Russia and other BRICS members have increased gold use for alternative settlement methods and continue talks on a regional precious metals exchange to expand non-dollar clearing.

Those policies shift some official reserves away from dollar assets and they raise the incentive to hold bullion globally.

RECOMMENDED: 5 Reasons to Buy Gold in 2025

Market Signals: Dollar, Real Rates, Supply Dynamics

Market signals offer clear catalysts. The dollar has fallen about 10% this year, and gold has risen roughly 37% in 2025 as markets price Fed easing. Lower US real yields lower the opportunity cost of non-yielding bullion.

Q1 mine output stood at 855.7 tonnes, with recycling steady, tightening available supply. That combination magnifies price moves when official and investor demand grows.

There are, however, risks such as sudden policy surprises, hot inflation prints, and disclosure lags that can amplify volatility in short order.

RECOMMENDED: Key Differences of Currency vs Gold Trading

Conclusion

Structural reserve shifts and sustained official buying create a fertile backdrop for further gold gains, but short-term shocks can interrupt. If you are planning to invest in gold, watch central-bank flows, DXY moves, and US real yields closely.

Stay Ahead of the Market – Get Premium Alerts Instantly

Join the original market-timing research service — delivering premium insights since 2017. Our alerts are powered by a proprietary 15‑indicator system refined over 15+ years of hands-on market experience. This is the same service that accurately guided investors through stock market corrections and precious metals rallies.

Act now and discover why thousands rely on us for timely, actionable signals — before the market makes its move.

Here’s how we’re guiding our premium members (log in required):

- Monster Basing Patterns in Precious Metals Resolving Higher (Sept 6th)

- Must-See Monthly Gold & Silver Charts (Aug 31)

- The 5 Most Important Silver Charts For H2/2025 (Hint: Very Bullish) (Aug 23)

- Silver – Speculators Keep Exiting The Long Side. What Does It Mean?(Aug 16)

- Must-See Secular Charts: Precious Metals Mining Breakout & More (Aug 9)

- The Monthly Silver Chart Looks Good + A Special Harmonic Setup On The EURUSD (Aug 2)